Payment card processing involves many steps and processes carried out by the parties involved. Merchants pay fees to accept payment cards and for the services provided to them by acquiring banks and processors. Acquirers and issuers must set up and maintain systems for the card processing and messages exchange through the card networks. Building and maintaining the card schemes and systems are costly. So the different parties must make some money to stay in business and keep providing the services. In this article, we will consider the payment card processing fees and see how they are distributed in the Four Corner Model.

Card payment transactions start with Merchants. They are the end customers of the whole system, the ones who want and who benefit from the card processing services. But accepting credit cards implies some costs that merchants obviously have to consider when setting the prices of goods or services that they sell. Among others, there are:

-

The cost of the PoS terminal (or Payment Gateway for e-merchants): It is up to the merchant to equip himself with a card machine. Acquirers generally offer terminals alone or in bundled offerings. But merchants do not have to take it from them. In many countries, card machines can be bought from approved manufacturers. There are different types of PoS terminals that have more or less sophisticated functions. The price can vary from one to the

-

Costs to set up the service

-

Costs for additional services (multiple cards acceptance, security and anti-fraud, maintenance, and so on).

-

Costs due to disputes and fraud

-

Variable costs in case of non-compliance with terms and conditions (e.g. late remittance of transactions)

- Merchant account commissions

-

Merchant Discount Rate: it will be analyzed in detail below.

-

Etc.

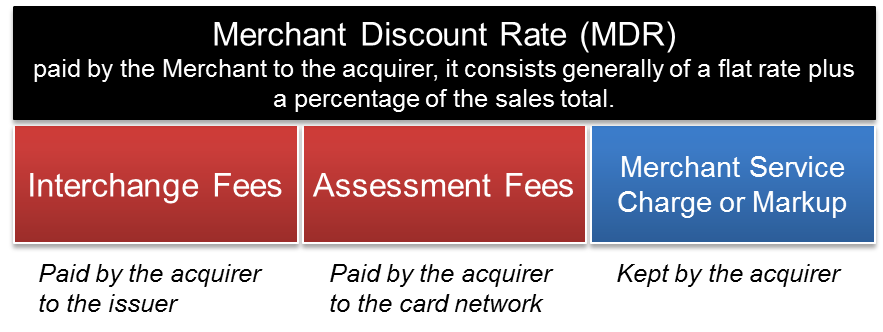

Merchants pay a rate on each card transaction amount for the payment processing. That rate is called the Merchant Discount Rate. It consists of several components visible on the next figure.

The components of the Merchant Discount Rate

The Merchant Discount Rate can be split in the following three main parts:

- Interchange Fee

- Assessment Fee

- Merchant Service Charge or Markup

The Interchange Fee

This fee is paid by the acquiring bank or acquiring processor to the issuing bank. So it is settled between banks. The interchange fee participates in covering the costs caused by a payment card transaction. It is a compensation to the issuer for the services that it provides to the merchant’s bank or acquirer. These include debits and credits management on accounts, clearing, settlement, guarantee of payment, or the participation in the costs of collective measures of security and the fight against fraud.

The Assessment Fee

Payment card networks take this fee for transactions that are made with their branded cards. These fees are used to support the following functions:

- Network operations involved in running transactions

- Research and development into new fraud-prevention technologies

- Marketing expenses

- The setting of prices and rules

The assessment fee usually is based on a percentage of the total transaction volume for the month. It cannot be negotiated by merchants. Assessments fees are generally charged per transaction and may vary depending on the type of card and the pricing model that the merchant follows. For example, Visa charges 0.13% assessment rate for credit cards and 0.11% for debit cards. MasterCard charges 0.1275% for both credit and debit cards, but will slightly increase it to 0.13% effective April 8, 2018. American Express charges 0.15%.

The Merchant Service Charge or Markup

Acquiring banks and acquiring processors include a Merchant Service Charge or Markup over interchange fees and assessments to cover the cost of facilitating credit card transactions and also to make some profit. In many countries, this charge amounts to between 20% and 25% of total card-processing costs. In contrary to Interchange and assessment fees, Merchant Service Charges can be negotiated with the acquirers. Markup fees are different from processor to processor and may also include other types of fees. A merchant should understand (not always easy) and compare them carefully before deciding which processor to take as a partner.

Merchant Discount Rate Distribution in the Four Corner Model

Let’s now consider an example of a CAD 100 transaction initiated in a store in Canada. How much does the merchant pay for the transaction processing and what revenue does each party get?

Accepting card payments is necessary nowadays to get access to more customers, but this leads to costs that are far from negligible, especially for small merchants. The amount of interbank payment fees have fallen considerably in some regions because of regulatory pressures. Merchants however are not the only ones to pay for card processing and related services. Cardholders bear some of the costs too as we will see in the next article.

{kind=link}