Many take payment systems for granted and some are not even aware of their existence. But the reality is that our world would be completely different without them. What is a payment? What are payment instruments and payment systems? To start with fundamentals, this first article provides a brief introduction to payments and payment instruments and systems in general. Read on to find answers to the above questions.

What is a payment?

Put simply, a payment is a transfer of funds or monetary value. A payment transaction involves two end parties: On one side, the debtor or payer who sends the funds, and on the other side, the creditor or payee who receives the funds. An end party can be the sender or receiver of the payment. It is a party involved in any side of a payment transaction. Payments are generally made in exchange for the provision of goods, services between end parties, or to meet legal obligations.

What are payment instruments?

In the expression “payment instruments”, the word instrument immediately catches our attention. Let’s look at its definition and see how to combine it with payment. An instrument is defined as a means whereby something is achieved, performed, or furthered. It can be compared to a tool that aids in accomplishing a task. Tools make things very easy. You can do gardening or cooking without tools, spending a huge amount of time to eventually achieve pretty limited results. But how easy things are when you have the proper tools. Likewise, payment instruments facilitate payments and make fund transfers easy between the end parties involved.

Payment instruments can be divided in two categories: cash payment instruments and non-cash payment instruments. Cash is money in the physical form of currency, such as banknotes and coins. We are all used to it and use it, but it is probably the less understood payment instrument as we will see in future articles. Cash, unlike non-cash payment instruments, can be used anonymously on the part of both payer and payee and that makes it truly unique.

Non-cash payment instruments are multiple: Checks, Cards, Credit Transfers, Direct Debits, e-Money, Bitcoin, Ripple, etc. As providers of most of these payment instruments, banks and other financial institutions play a crucial role in payments. They hold depository accounts opened by End parties, consumers and businesses. Nowadays, a payment consists most of the time in transferring monetary value stored in depository accounts from one end party to another.

What are payment systems?

The banks connect to various payment systems in order to process and settle payments on behalf of their customers (and also for themselves). A payments system is a set of payment instruments, processes and, usually, interbank fund transfer systems that enable and guarantee the circulation of funds. It operates within a single country (or region) and, this is a key point, transactions are settled in the currency of that country. A currency is closely tied to a country, its government and its banking system. When two or more countries share the same currency, they build a monetary area or union and generally share the same payment systems. Since payment systems play a fundamental role in an economy, they are of particular interest to governments. In fact, payment systems are subject to regulation by the government of the country in which they operate. Participants in a payment system, generally banks, are bound by the rules. They must comply with the regulatory requirements and other specific payment system rules. Finally, there is a risk associated with settlement for the participants that a payment system is expected to manage partially or totally.

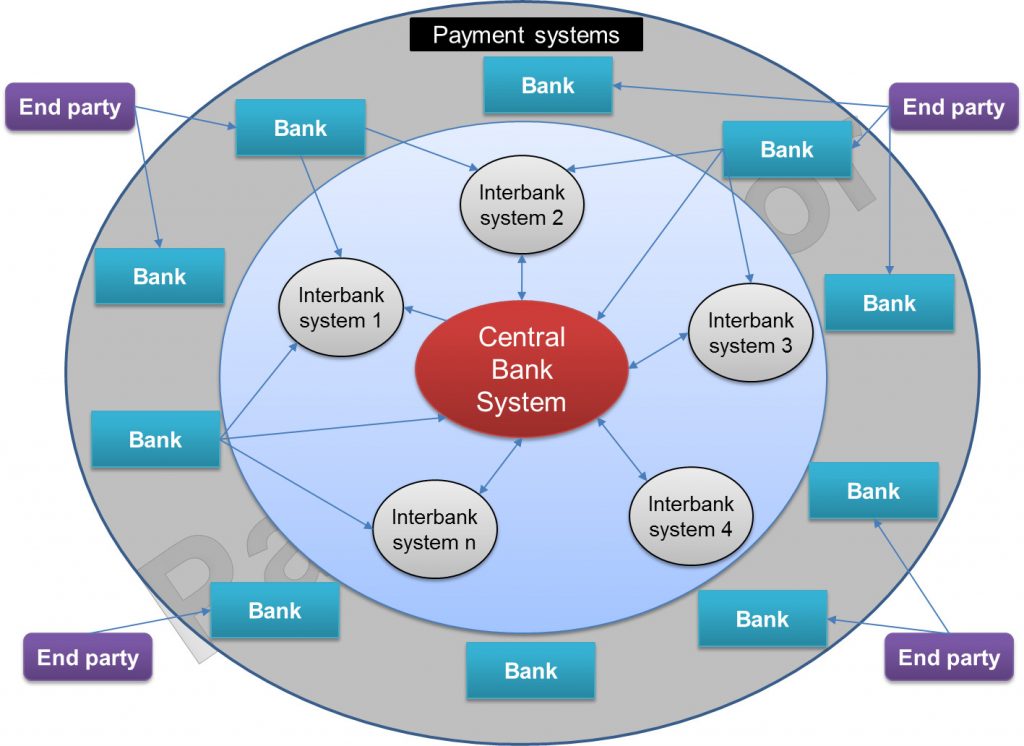

Traditional payment systems are modeled as a network composed of banks and similar financial institutions, interbank clearing systems (generally called ACH) and central bank systems. A payment transaction begins and ends with end parties and the funds transfer happens through banks and other intermediaries which are connected through interbank or central bank systems. The model depicted below is a very general one and can be used to explain many things. However, there are a few exceptions that will be examined in the future. It is a way to ensure you come back to the blog to read future posts.

Now let’s consider the different components of the model. Outside of the payment systems, you see end parties which are the consumers and businesses. End parties can be customers of one or more banks. An end party can open as many depository accounts with as many banks as it wants. The banks are participants to many interbank systems and to the central bank system for the clearing and settlement of their payment transactions. They can participate as direct or indirect participants and they obviously play the roles of intermediaries between interbank systems and end parties.

The central bank system is positioned in the middle of the model. That emphasizes the important role played by the central bank as overseer of the banking and monetary systems in a country or monetary zone. The final settlement of claims originating from interbank operations is performed in the central bank system, considered as the core payment system whereas interbank systems are considered as ancillary systems.

One remark: In the literature, the expression “payment systems” may be used for Interbank systems only or for central systems only or for the whole systems presented in the model and even more. So be careful when you read books or articles about payment systems.

Now you may wonder why banks need to connect to multiple systems to process and settle their payment transactions. There are two main reasons for it.

First, payments are classified in low-value payments or large/high-value payments. There are different processes and risk management associated with each category. This has led in many countries to the implementation of various systems to effectively and efficiently address the needs pertaining to each category of payments.

Second, in many countries, for historical reasons distinct systems were developed for the interbank exchange of messages related to the different payment instruments. Bank had to connect to the various systems to provide clearing and settlement services to their client over the whole set of payment instruments.

There are hundreds of payments systems around the world. Some are known only in their country (or region) of origin. Some are known all over the world. Look at the picture below. It contains logos of some payment systems. You have certainly recognized a few.

Cards payment systems like Visa, MasterCard or American express have a strong brand and are well known to the public. Union Pay is the Chinese Card system which has become very popular in the world with the growing economy of China. Unlike card systems, many payments systems are known only to professionals.

Fedwire and Nacha are respectively the large-value and low-value payment systems of the USA. Transactions are therefore settled in USD currency. Fedwire is owned and operated by the Federal Reserve Bank. In addition to Fedwire, there is another payment system used to settle wire transfers with very high amounts in the USA: CHIPs. It is operated by the Clearing House. Nacha is used for the interbank exchanges of low value payments through checks, credit transfers, direct debits and other similar payment instruments.

TARGET2 is the large-value payment system of the Eurozone. It is operated by the European Central Bank (ECB). EBA Clearing is an interbank payments corporation which operates EURO1 / STEP1 (equivalent to CHIPs in the USA) for large-value payments, STEP2 for low-value payments, IPS for instant payments. STET is a French corporation offering interbank fund transfers services for low-value payments in France and Belgium through a system called Compensation REtail (CORE). It is interesting to note that Banks in France and Belgium are also participants of EBA Clearing systems and TARGET2. TARGET2, EURO1 / STEP1, STEP2, IPS and CORE process and settle transactions in EUR currency.

BACS, Faster Payments and CHAPs systems are all UK systems which facilitate fund transfers in the local currency, the GPB. BACS is the low-value payment system. Faster Payments is the instant payment system and CHAPs is the large-value payment system.

Paypal, Facebook Messenger payments, Google Wallet, Apple pay and Bitcoin can all be considered as low-value payment systems. All of them except Bitcoin extensively rely on services provided by low-value payment systems for fund transfers. We will describe in detail how they work in next articles.

Traditional payment systems are grounded on centralized models. In the recent years, technology has enabled the emergence of payment systems based on models which are decentralized. Non-traditional payment systems such as Bitcoin do not rely on the current banking system for the exchange of values. They do not operate within a country and but directly over the Internet. They are used for the exchange of digital currencies almost without intermediaries.

In summary, a payment is a transfer of funds or monetary value. Payment instruments were created to ease the transfer of funds between end parties. They are offered by Banks which connect to various payment systems to exchange and settle funds in the currency of their country or region. In the next article, we will look at Payment systems models.

In the Payment System explanation you have mentioned ACH as Inter Bank Clearing System..But isnt ACH typically related to the electronic transactions or transfers that happen using the ACH network, mostly in US?

Even in that case we have Fed Reserve or EPN serving as the Clearing Houses or ACH Operators.

Or is ACH used at liberty even while talking about any Clearing House in general?

Hi Jean

So payment systems like Visa and MasterCard provide clearing and settlement infrastructure to the banks for processing and settling their payment transactions? How is the CSM provided by Visa/ MasterCard different to the CSM connected to central bank?

Could you please clarify?

[…] Payment Instruments […]